RESOURCES

for enhancing financial knowledge

SPRING 2023

Before you bond with your newborn, newly adopted or foster child, you’ll need to do some math. The overall cost of raising children in the United States aside (~$17,000 each year, per child), some of the first financial conversations soon-to-be parents have will revolve around childcare needs, from those first precious weeks through formal schooling.

And what a sobering conversation that can be. Although the Federal Employee Paid Leave Act granted federal employees 12 weeks of paid parental leave, those employed by small businesses, self-employed or part of nontraditional work arrangements don’t qualify.

This means they must rely on either their state or company’s policy, or the Family and Medical Leave Act (FMLA) – where companies with 50 employees or more are required to provide up to 12 weeks of job-protected, unpaid time off – for any chance at a patchwork plan and that only covers 56% of U.S. workers.

However, many can’t afford to take unpaid leave and only nine states and the District of Columbia offer paid family leave programs. What’s more, only 19% have defined benefits through their employer … a number that shrinks further among low-wage and hourly workers.

Among companies that do provide paid parental leave, leading the way are technology, financial services, insurance, and professional services industries, with leisure and hospitality industry lagging far behind. No matter where companies fall on the spectrum, time available is wide – Netflix provides 52 weeks of paid parental leave and Boeing gives three weeks, for example.

Changing public attitudes and the difficulty of balancing work and family in today’s economy contribute to an increasing sense of urgency around what’s next for paid family leave in the U.S.

These days, it’s likely that all adults work in the standard American household. Without a parent at home, there’s little flexibility for home-based care for a new baby, sick child or elderly relative without putting jobs in jeopardy.

Millennials facing the lack of paid parental leave and high childcare costs are changing their life plans and having fewer kids than they want.

When it comes to parenting and work, millennials differ from previous generations, which may affect future policy decisions around paid family leave.

Source: Ernst and Young. Study: Work-Life Challenges Across Generations. 2015

Unfortunately, the U.S. is lacking a national paid parental leave policy compared to, well, just about every other country. As of November 2021, we’re the only wealthy country without guaranteed paid parental leave at the national level, based on data from the World Policy Analysis Center.

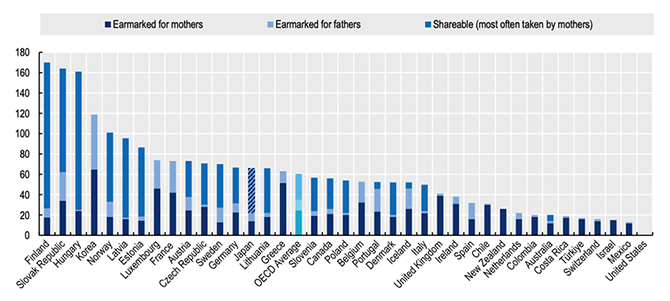

Across Organisation for Economic Co-operation and Development (OECD) countries, mothers are entitled to just above 32 weeks on average for paid parental and home care. However, 11 OECD countries offer no such leave. While some countries provide more than six months of paid maternity leave, the average is just under 19 weeks. New fathers average just above 10 weeks of paid leave.

Some countries allow paid family leave to be shared between parents. Although mothers take the majority, the other partner can use parts of their collective entitlement – on average 25.4 weeks for OECD countries.

Length in weeks of shareable paid family leave, 2022

Finland, Hungary and the Slovak Republic provide a shareable 2 1/2 years of paid leave or more. Source: Organisation for Economic Co-operation and Development

Research shows the benefits of paid leave on physical and mental health, and family stability. The American Psychological Association reported that paid parental leave can reduce financial stress, empower parents to focus on bonding with their kids, and increase gender equality when fathers are provided time to share in childcare duties.

More collaboration between psychologists and economists could help quantify outcomes – such as reduced healthcare costs, more happiness, job retention – in a way that’s meaningful on a policy level.

Before heading overseas to start your family, consider:

Sources: Center on Budget and Policy Priorities; National Institutes of Health; American Psychological Association; Organisation for Economic Co-operation and Development; Bipartisan Policy Center; U.S. Bureau of Labor Statistics

There are times when we all feel “less than” in different facets of our lives. Turns out those feelings of insecurity and self-doubt have infused themselves into the collective consciousness of many professionals – time and time again.

In a 2020 KPMG study of 750 executive women from major companies, the firm found that 75% experienced imposter syndrome in their careers. And not just once.

The study found that feelings of inadequacy appeared during pivotal moments in an existing role or during promotions or career changes. This makes sense since imposter syndrome has been defined as “the inability to believe your success is deserved as a result of your hard work and the fact you possess distinct skills, capabilities and experiences.”

A Harvard Business Review article states that imposter syndrome disproportionately affects high-achieving people, who find it difficult to accept their accomplishments. But, of course, your success doesn’t stem from luck.

Those doubts don’t have to overshadow your ability to continue thriving.

Nearly half of the women from the KPMG survey never expected to be as successful as they are, causing self-doubt – and more than half have been scared they can’t live up to expectations.

One way that almost three-quarters of surveyed women regained confidence was by seeking advice from a mentor when they doubted their abilities to take on new roles.

Having strong relationships with colleagues and leaders fosters a culture where women feel empowered to turn fears into growth opportunities. In fact, 47% believe having a supportive performance manager is the most important factor to combat imposter syndrome.

With teamwork and an inclusive culture, all professionals can feel respected and valued, collectively moving one step closer to promoting self-worth over self-doubt.

Sources: “Advancing the Future of Women in Business: A KPMG Women’s Leadership Summit Report” a survey of 750 executive women from major companies, 2020; Harvard Business Review; forbes.com

“Not all those who wander are lost.” – J. R. R. Tolkien

When it comes to solo international travel, some bristle at the thought of taking a journey alone – and others can’t wait to strap into their overnight flight and step into a new adventure.

Pre-pandemic, only 14% of travelers were going solo, but that number almost doubled mid-2021, according to Booking.com. Even before COVID-19, Google searches for “solo female travel” increased – 230% in 2019 per worldpackers.com. And most of the world is now open for travel, at least for vaccinated travelers and those who pass pre-arrival COVID-19 tests in some destinations.

The pandemic left us more self-aware … ready to get out of our heads and into new experiences. Whether you’re tired of waiting for a travel buddy or are ready to check out a new destination that includes me time, a solo journey is an act of self-love worth pursuing.

Choose your destination with the intent to let go of worries and go all in on your new surroundings. Last fall, Travel & Leisure named these 12 international destinations as the best trips for solo female travelers:

No matter where you jet off to, be prepared and have a plan – even if that means a framework with room for spontaneity. Nobody wants unexpected adventures to take a dark turn, so in addition to following basic travel safety, these tips can help when you’re on your own:

And it’s still a good idea to bring a mask in your carry-on since some locations still have indoor mask mandates.

So, book that flight. You may find that even though you started this journey alone, you come home with a new sense of confidence and contacts in your phone from like-minded solo travelers to plan your next adventure with.