RESOURCES

for enhancing financial knowledge

The reaction from markets to the release of Q1 2024 real GDP results has given every sector of the market another chance to give their own interpretation of what is coming regarding Federal Reserve (Fed) policy, inflation, and the federal funds rate. We have already started to hear that the Fed is not going to cut rates at all during the year; that it is only going to cut twice, or just once; that we are going into a stagflation process (we thought we had made the case clear that the current process has no similarities to the stagflation process of the 60s, 70s, and early 80s), just because of a worse than expected quarterly PCE price index number; that we are going into a recession because the yield curve has been inverted for too long, etc. In fact, the latter group – yield curve inversion group – has been consistent over time.

The only problem with some of this group’s thinking today is that while in the past they have argued for a recession and immediate interest rate cuts by the Fed, they seem to have jumped onto the ‘stagflation’ bandwagon, which argues that we will have a recession but with much higher inflation and no rate cuts. And then, there are those calling for the Fed to actually increase interest rates under the argument that it stopped rising interest rates too early.

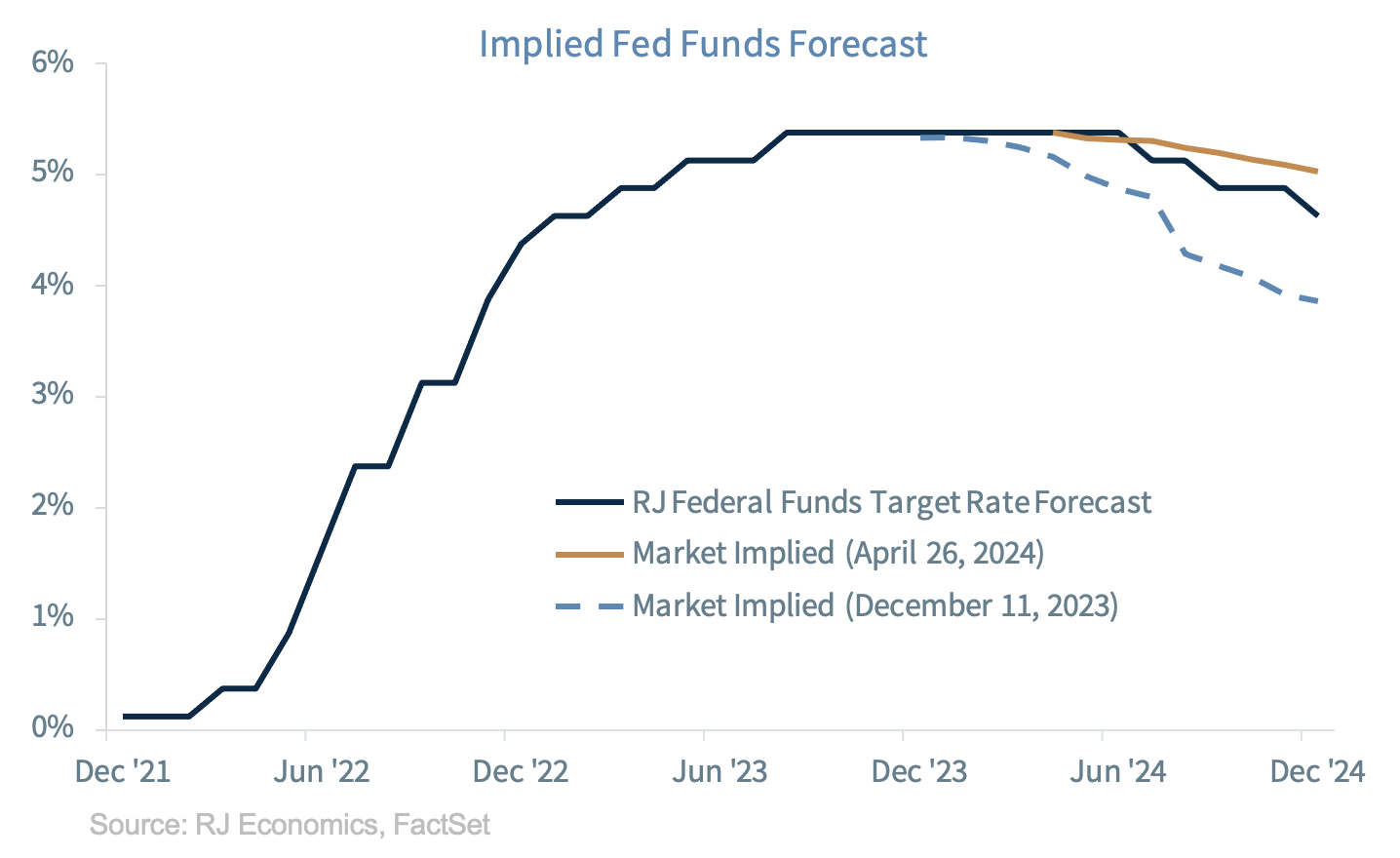

What is important to remember is that this was the same market that was pricing in seven interest rate cuts in 2024 just four months ago!!

It is true that the rate of inflation during the first quarter of the year is not what markets were expecting, but we always said that the last stretch of the disinflationary process was going to be a long one. The Fed knows this, that is the reason why it expects to hit the 2% target in 2026, not today, not this year, not even in 2025. There is plenty of time for Fed policy to work its magic and the Fed has positioned itself to do that. It is true that the worse than expected result in the first quarter may delay the decision to start cutting interest rates to later this year. Please see the section on the following page where we discuss our changes. The truth is that nothing else has really changed from what we were expecting earlier this year or even last year.

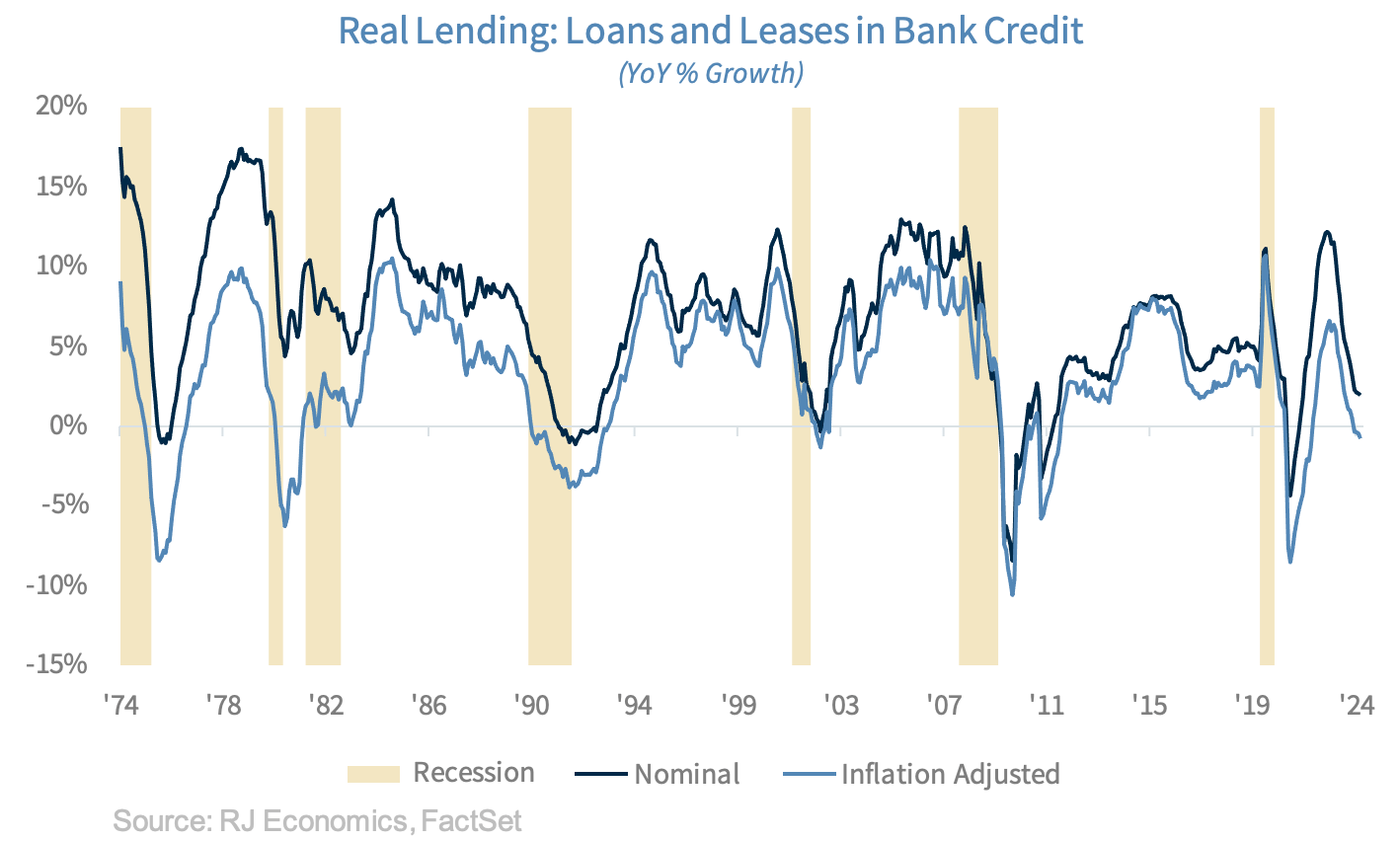

Our expectation for the disinflationary process to continue during the year remains intact. Thus, the Fed will achieve its goals with current interest rates so there is no need to increase interest rates further, as some have started to speculate. Lending is almost flat and even credit card lending has started to weaken, which was the only component of lending that remained a concern for the Fed, as the graph below clearly shows. Furthermore, real money supply growth has remained in negative territory, which is what the Fed needs to keep inflation on its disinflationary path.

Perhaps one of the potential arguments for the Fed to increase interest rates today is if it wants to slow consumption, as higher interest rates increase the trade-off between consuming today versus consuming tomorrow. However, the Fed doesn’t need to do that today because long term interest rates are moving higher anyway even as the Fed has kept the federal funds rate fixed. And this, if sustained, should do the trick for the Fed. Thus, even that argument for higher interest rates is not a compelling one today.

Furthermore, today’s monthly personal income and consumption report for March confirmed our suspicions that yesterday’s 1Q GDP report was a ‘nothingburger’ and that the Fed, and markets, should Keep Calm and Carry On!

After considering the higher than expected inflation print during the first quarter of the year we are making a slight change to our federal funds rate forecast. We are keeping, for now, our call for three rate cuts but we are changing our expectation for the first Fed cut to July rather than June. This will give us an opportunity to see June’s dot-plot in order to gauge what effects, if any, first quarter inflation numbers have had on Fed members’ views on the policy target. Thus, we are now expecting cuts in the federal funds rate in July, September, and December.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those Raymond James and are subject to change without notice the information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur last performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the U.S. Bureau of Labor Studies. Currencies investing are generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

The National Federation of Independent Business (NFIB) Small Business Optimism Index is a composite of ten seasonally adjusted components. It provides a indication of the health of small businesses in the U.S., which account of roughly 50% of the nation's private workforce.

The producer price index is a price index that measures the average changes in prices received by domestic producers for their output. Its importance is being undermined by the steady decline in manufactured goods as a share of spending.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.